Many people I talk to believe that now is not a good time to sell a home. However, the purchase and sale of real estate happens everyday. There are always buyers in the market. The ones that are in the market at the end of the year tend to be highly motivated.

Real-life Example Time:

I listed a home one week ago. Within 1 day on the market, the home had 2 full-priced offers. It got a 3rd full-priced offer that became a back-up offer. There is still significant demand in the market.

I am always happy to speak with you about your real estate goals. Let me know how I can have a positive impact on your life.

Buyers looking right now are highly motivated, the supply of homes for sale is still low, and you may find buyers are more flexible with showings this time of year.

I have so many conversations with people that are worried about the institutional buyers snapping up homes and knocking the average homebuyer out of the market. Below is good information about the institutional buyer and rental homes.

Let me know whose life I can positively impact today. I am always available to answer your real estate questions and discuss your specific real estate goals.

Realtor Persephone Galambos

BHGRE Metro Brokers

404-429-6695

persephone.galambos@metrobrokers.com

Is Wall Street Buying Up All the Homes in America?

If you’re thinking about buying a home, you may find yourself interested in the latest real estate headlines so you can have a pulse on all of the things that could impact your decision. If that’s the case, you’ve probably heard mention of investors, and wondered how they’re impacting the housing market right now. That could leave you asking yourself questions like:

How many homes do investors own?

Are institutional investors, like large Wall Street Firms, really buying up so many homes that the average person can’t find one?

To answer those questions, here’s the real story of what’s happening based on the data.

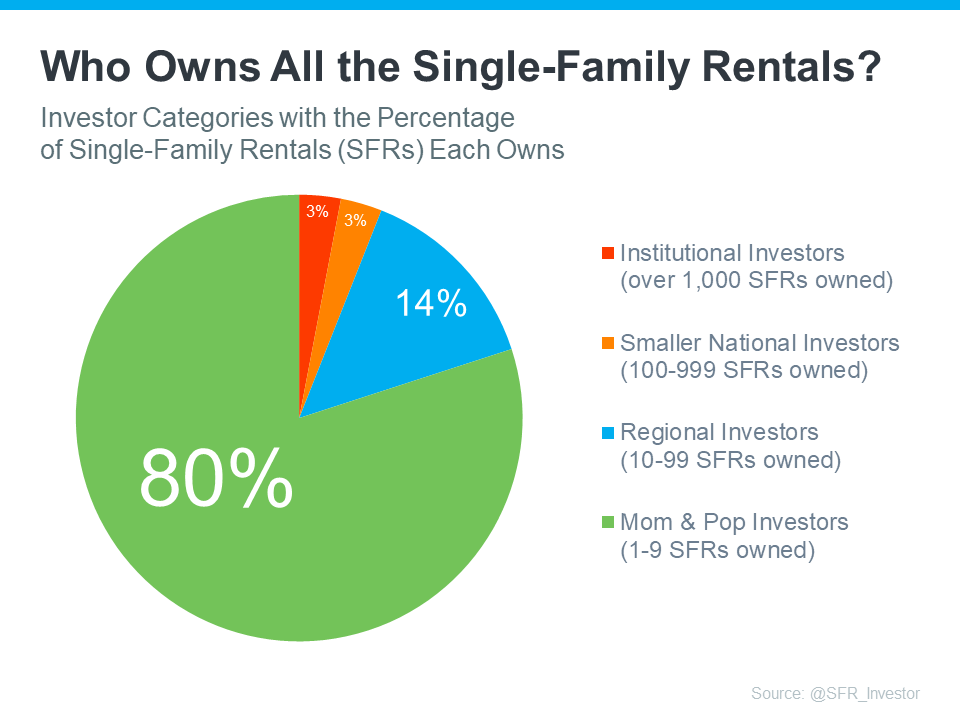

Let’s start with establishing how many single-family homes (SFHs) there are and what portion of those are rentals owned by investors. According to SFR Investor, which studies the single-family rental market in the United States, there are eighty-two million single-family homes in this country. But how many of them are actually rentals?

According to data shared in a recent post, sixty-eight million (82.93%) of those homes are owner-occupied – meaning the person who owns the home lives in it. If you subtract that sixty-eight million from the total number of single-family homes (82 million), that leaves just about fourteen million homes left that are single-family rentals (SFRs).

Do institutional investors own all of those remaining fourteen million homes? Not even close. Let’s take it one step further. There are four categories of investors:

The mom & pop investor who owns between 1-9 SFRs

The regional investor who owns between 10-99 SFRs

Smaller national investor who owns between 100-999 SFRs

The institutional investor who owns over 1,000 SFRs

These categories show that not all investors are large institutional investors. To help convey that even more clearly, here are the percentages of rental homes owned by each type of investor (see chart below):

As you can see in the chart, despite what the news and social media would have you believe, the green shows the vast majority are not owned by large institutional investors. Instead, most are owned by small mom & pop investors, like your friends and neighbors.

What’s actually happening is, that there are people out there, just like you, who believe in homeownership, and they view buying a home (or a second home) as an investment. Maybe they saw an opportunity to buy a second home over the last few years to use it as a rental and generate additional income. Or maybe they just decided to keep their first house rather than sell it when they moved up.

So, don’t believe everything you read or hear about institutional investors.They aren’t buying up all the homes and making it impossible for the average person to buy. That’s just not what the numbers show. Institutional investors are actually the smallest piece of the pie chart.

Bottom Line

While it’s true that institutional investors are a player in the single-family rental marketplace, they’re not buying up all of the houses on the market. If you have other questions about things you’re hearing about the housing market, let’s connect so you have an expert to give you the context you need.

I talk to so many people who are concerned about or waiting for the housing prices to collapse. Here is some information about places where the housing prices are still increasing (but at a slower rate than the past few years). Atlanta is right near the top due to the strong economy and strong housing demand.

I am always happy to discuss your specific real estate goals. Let me know how I can have a positive impact on your life.

Persephone Galambos, Realtor

BHGRE Metro Brokers

404-429-6695

persephone.galambos@metrobrokers.com

These Top Cities Show Home Prices Are Still Climbing

If you’re considering buying a home or selling your current one to find something that better suits your needs, you may have questions about what’s happening with home prices today. Here’s what you need to know.

There’s still a lot of confusion and misinformation out there. So, no matter what you may have heard, the national data shows they’ve actually been climbing again (see graphs below):

As you can see, in the first half of 2022, home prices went way up. Those increases were dramatic and unsustainable. So, in the second half of 2022, prices adjusted. Those dips were small and didn’t last very long. Still, the news made a big deal about these slight declines, which may have made you worry.

But what’s important to know is that, in 2023, prices are going up again, and this time it’s at a more normal pace. The fact that all three reports now show more typical price increases this year is good news for the housing market.

Home Prices Are Rising Across the Top Cities in the U.S.

After seeing steady home price growth at the national level for the last several months, you may wonder if prices are going up in your local area, too. Know this: while this will vary from one area to the next, home prices are appreciating in these top cities Case-Shiller reports on in their monthly price index (see chart below):

That’s why so many experts are able to forecast home prices will end the year in the positive and continue going up in 2024.

Here’s How This Affects You

For Buyers: If you’ve been waiting to buy a home because you were concerned it might lose value, the fact that home prices are going up should ease your worries. Buying a home before prices climb higher can be a smart move since home values typically appreciate over time.

For Sellers: If you’ve been postponing selling your house because you were worried about how changing home prices would affect its value, now might be a good time to work with a real estate agent to put your house on the market. You don’t have to wait any longer because the data shows home prices are in your favor.

Bottom Line

If you delayed moving because you were concerned home prices would drop, don’t worry – the numbers show they’re going up nationally. To better understand how home prices are changing in your local area, let’s connect.

I have multiple conversations each day with folks that do not want to make a real estate move because they believe housing prices will decline. Many also believe that foreclosures and short sales are going to increase.

There has been a slight increase in foreclosures/short sales. However, they are still below what is considered a normal rate of foreclosures. This article provides some excellent information about foreclosures/short sales.

I am always happy to answer your real estate questions. How can I touch your life positively today?

Realtor Persephone Galambos

BHGRE Metro Brokers

404-429-6695

persephone.galambos@metrobrokers.com

Foreclosures and Bankruptcies Won’t Crash the Housing Market

If you’ve been following the news recently, you might have seen articles about an increase in foreclosures and bankruptcies. That could be making you feel uneasy, especially if you’re thinking about buying or selling a house.

But the truth is, even though the numbers are going up, the data shows the housing market isn’t headed for a crisis.

Foreclosure Activity Rising, but Less Than Headlines Suggest

In recent years, the number of foreclosures has been very low. That’s because, in 2020 and 2021, the forbearance program and other relief options were put in place to help many homeowners stay in their homes during that tough time.

When the moratorium ended, there was an expected rise in foreclosures. But just because they’re up, that doesn’t mean the housing market is in trouble.

To help you see how much things have changed since the housing crash in 2008, check out the graph below using research from ATTOM, a property data provider. It looks at properties with a foreclosure filing going all the way back to 2005 to show that there have been fewer foreclosures since the crash.

As you can see, foreclosure filings are inching back up to pre-pandemic numbers, but they’re still way lower than when the housing market crashed in 2008. And today, the tremendous amount of equity American homeowners have in their homes can help people sell and avoid foreclosure.

The Increase in Bankruptcies Isn’t Dramatic Either

As you can see below, the financial trouble many industries and small businesses felt during the pandemic didn’t cause a dramatic increase in bankruptcies. Still, the number of bankruptcies has gone up slightly since last year, nearly returning to 2021 levels. But that isn’t cause for alarm.

The numbers for 2021 and 2022 were lower than more typical years. That’s in part because the government provided trillions of dollars in aid to individuals and businesses during the pandemic. So, let’s instead focus on the bar for this year and compare it to the bar on the far left (2019). It shows the number of bankruptcies today is still nowhere near where it was before the pandemic. Both of these two factors are reasons why the housing market isn’t in danger of crashing.

Bottom Line

Right now, it’s crucial to understand the data. Foreclosures and bankruptcies are rising, but these leading indicators aren’t signaling trouble that would cause another crash.

I have a lot of conversations about the state of the real estate market. Many people would like to move but are put off by the mortgage rates.

Something to think about when making a decision is that the high mortgage rates are causing a tremendous amount of pent up demand. When rates do start to come down, that demand will be released on the market. It will likely create a run up in prices. While there is little that can mitigate pricing increases caused by demand, there can be opportunities to refinance a mortgage from a higher interest rate to a lower interest rates when rates come down.

It is something to consider when deciding if a real estate purchase is right for you. I am always available to discuss your real estate questions and needs.

Whose life can I touch today in a positive way?

Persephone Galambos, Realtor BHGRE Metro Brokers 404-429-6695 persephone.galambos@metrobrokers.com

Are Higher Mortgage Rates Here To Stay?

Mortgage rates have been back on the rise recently and that’s getting a lot of attention from the press. If you’ve been following the headlines, you may have even seen rates recently reached their highest level in over two decades (see graph below):

That can feel like a little bit of a gut punch if you’re thinking about making a move. If you’re wondering whether or not you should delay your plans, here’s what you really need to know.

How Higher Mortgage Rates Impact You

There’s no denying mortgage rates are higher right now than they were in recent years. And, when rates are up, that affects overall home affordability. It works like this. The higher the rate, the more expensive it is to borrow money when you buy a home. That’s because, as rates trend up, your monthly mortgage payment for your future home loan also increases.

Urban Instituteexplains how this is impacting buyers and sellers right now:

“When mortgage rates go up, monthly housing payments on new purchases also increase. For potential buyers, increased monthly payments can reduce the share of available affordable homes . . . Additionally, higher interest rates mean fewer homes on the market, as existing homeowners have an incentive to hold on to their home to keep their low interest rate.”

Basically, some people are deciding to put their plans on hold because of where mortgage rates are right now.But what you want to know is: is that a good strategy?

Where Will Mortgage Rates Go from Here?

If you’re eager for mortgage rates to drop, you’re not alone. A lot of people are waiting for that to happen. But here’s the thing. No one knows when it will. Even the experts can’t say with certainty what’s going to happen next.

Forecasts project rates will fall in the months ahead, but what the latest data says is that rates have been climbing lately. This disconnect shows just how tricky mortgage rates are to project.

The best advice for your move is this: don’t try to control what you can’t control. This includes trying to time the market or guess what the future holds for mortgage rates. As CBS Newsstates:

“If you’re in the market for a new home, experts typically recommend focusing your search on the right home purchase — not the interest rate environment.”

Instead, work on building a team of skilled professionals, including a trusted lender and real estate agent, who can explain what’s happening in the market and what it means for you. If you need to move because you’re changing jobs, want to be closer to family, or are in the middle of another big life change, the right team can help you achieve your goal, even now.

Bottom Line

The best advice for your move is: don’t try to control what you can’t control – especially mortgage rates. Even the experts can’t say for certain where they’ll go from here. Instead, focus on building a team of trusted professionals who can keep you informed. When you’re ready to get the process started, let’s connect.

An important factor shaping today’s market is the number of homes for sale. And, if you’re considering whether or not to list your house, that’s one of the biggest advantages you have right now. When housing inventory is this low, your house will stand out, especially if it’s priced right.

But there are some early signs that more listings are coming. According to the latest data, new listings (homeowners who just put their house up for sale) are trending up. Here’s a look at why this is noteworthy and what it may mean for you.

More Homes Are Coming onto the Market than Usual

It’s well known that the busiest time in the housing market each year is the spring buying season. That’s why there’s a predictable increase in the volume of newly listed homes throughout the first half of the year. Sellers are anticipating this and ramping up for the months when buyers are most active. But, as the school year kicks off and as the holidays approach, the market cools. It’s what’s expected.

But here’s what’s surprising. Based on the latest data from Realtor.com, there’s an increase in the number of sellers listing their houses later this year than usual. A peak this late in the year isn’t typical. You can see both the normal seasonal trend and the unusual August in the graph below:As Realtor.comexplains:

“While inventory continues to be in short supply, August witnessed an unusual uptick in newly listed homes compared to July, hopefully signaling a return in seller activity heading toward the fall season . . .”

While this is only one month of data, it’s unusual enough to note. It’s still too early to say for sure if this trend will continue, but it’s something you’ll want to stay ahead of if it does.

What This Means for You

If you’ve been putting off selling your house, now may be the sweet spot to make your move. That’s because, if this trend continues, you’ll have more competition the longer you wait. And if your neighbor puts their house up for sale too, it means you may have to share buyers’ attention with that other homeowner. If you sell now, you can beat your neighbors to the punch.

But, even with more homes coming onto the market, the market is still well below normal supply levels. And, that inventory deficit isn’t going to be reversed overnight. The graph below helps put this into context, so you can see the opportunity you still have now:

Bottom Line

Even though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. You still have an incredible opportunity if you sell your house today. Let’s connect to explore the benefits of selling now before more homes come to the market.

I am having a lot of conversations on this topic. It is heavy on homeowners and potential homeowners alike.

First time homebuyers are wondering if they should just wait until housing prices come down. Homeowners that purchased recently are worried if they have the potential to be upside down in their home equity.

Economists seem to have a general consensus that home prices will continue to increase over the next 5 years. Housing demand is a big factor in this since new home construction has been lagging behind demand for years and cannot catch up.

I am always happy to speak with you about your specific situation and provide information that will assist you in making informed decisions on one of your largest assets.

Persephone Galambos, Realtor

Better Homes and Garden Real Estate Metro Brokers

404-429-6695

persephone.galambos@metrobrokers.com

What Experts Project for Home Prices Over the Next 5 Years

If you’re planning to buy a home, one thing to consider is what experts project home prices will do in the future and how that might affect your investment. While you may have seen negative news over the past year about home prices, they’re doing far better than expected and are rising across the country. And data shows, experts forecast home prices will keep appreciating.

Experts Project Ongoing Appreciation

Pulsenomics polled over 100 economists, investment strategists, and housing market analysts in the latest quarterly Home Price Expectation Survey (HPES). The results show what the panelists project will happen with home prices over the next five years. Here are those expert forecasts saying home prices will go up every year through 2027 (see graph below):If you’re someone who was worried home prices would fall because of stories you’ve read online, here’s the big takeaway. Even though home prices vary by local market, experts project prices will continue to rise across the country for years to come. And these numbers indicate the return to more normal home price appreciation.

And while the projected increase in 2024 isn’t as large as 2023, it’s important to recognize home price appreciation is cumulative. In other words, if these experts are correct, after your home’s value rises by 3.32% this year, it’ll appreciate by another 2.17% next year. This is a good example of why owning a home is a choice that wins big over time.

What Does This Mean for You?

Once you buy a home, price appreciation raises your home’s value, and that grows your household wealth. To see how a typical home’s value could change in the next few years using the expert projections from the HPES, check out the graph below:In this example, let’s say you bought a $400,000 home at the beginning of this year. If you factor in the forecast from the HPES, you could potentially accumulate more than $71,000 in household wealth over the next five years.

So, if you’re thinking about whether buying a home is a good choice, remember how it can be a powerful way to grow your wealth in the long run.

Bottom Line

According to the experts, home prices are expected to grow over the next five years at a more normal pace. If you’re ready to become a homeowner, know that buying today can set you up for long-term success as home values (and your own net worth) grow. Let’s connect to start the homebuying process today.

Many news headlines can be radical. They are written to get attention. Full-time Realtors are out in the local market everyday. Good Realtors also keep up with local and national real estate news. Informed Realtors can assist real estate investors/homeowners in making decisions that are best for them.

Metro-Atlanta has seen strong population growth over the past several years (Cherokee County was the fastest growing county in the state of Georgia over the past year). The strong and diverse economy has contributed to this strong growth. This is not anticipated to change in the near future. This means that the metro-Atlanta area will continue to have ongoing housing demand.

Renters have limited control over their housing budget from year to year. Homeowners have a relatively stable housing cost that is primarily affected by property taxes and homeowners insurance. Repairs are part of the cost of homeownership that need to be planned for either with savings and/or a home warranty.

I am always happy to answer any questions you may have regarding your real estate goals.

Persephone Galambos, Realtor

Better Homes and Gardens Real Estate Metro Brokers

404-429-6695

persephone.galambos@metrobrokers.com

Why You Need a True Expert in Today’s Housing Market

The housing market continues to shift and change, and in a fast-moving landscape like we’re in right now, it’s more important than ever to have a trusted real estate agent on your side. Whether you’re buying your first home or selling once again, it’s mission critical to work with an expert who can guide you through each unique step of the process.

The reality is, not all agents operate the same way. To truly make a powerful and confident decision as you buy or sell a home, you need a real estate expert who uses their knowledge of what’s really happening with home prices, housing supply, industry projections, and more to give you the best possible advice. Someone who can provide clarity and trust like that is essential to your success. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty for consumers. As Jason Lewris, Co-Founder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying a home is a big decision, and it should be one you feel confident making. You can lean on an expert to help you separate fact from fiction and get the answers you need.

The right agent can assist you in figuring out what’s going on at the national level and in your local area. They can debunk headlines using data you can trust. Experts have in-depth knowledge of the industry and can provide context, so you know how current trends compare to the normal ebbs and flows in the housing market, historical data, and more.

Then, to make sure you have the full picture, an agent can tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you can use all that information to make the best possible decision.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where a trusted expert comes in.

Bottom Line

If you want sound advice and trusted information about our local housing market, let’s connect.

Pricing a home correctly is vitally important to a successful home sale that nets a homeowner the most money possible in a transaction.

I was a commercial appraiser for 14 years prior to becoming a Realtor. I am always happy to speak with you about your homes value based on your specific home in the current market. Always feel free to reach out to me with any of your real estate questions.

While this isn’t the frenzied market we saw during the ‘unicorn’ years, homes that are priced right are still selling quickly and seeing multiple offers right now. That’s because the number of homes for sale is still so low. Data from the National Association of Realtors (NAR) shows 76% of homes sold within a month and the average saw 3.5 offers in June.

To set yourself up to see advantages like these, you need to rely on an agent. Only an agent has the expertise needed to find the right asking price for your house. Here’s what’s at stake if that price isn’t accurate for today’s market value.

The price you set for your house sends a message to potential buyers.

Price it toolow and you might raise questions about your home’s condition or lead buyers to assume something is wrong with it. Not to mention, if you undervalue your house, you could leave money on the table, which decreases your future buying power.

On the other hand, price it too high and you run the risk of deterring buyers from ever touring it in the first place. When that happens, you may have to do a price drop to try to re-ignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder why the price was reduced and what that means about the home.

“Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing . . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house.”

Think of pricing your home as a target. Your goal is to aim directly for the center – not too high, not too low, but right at market value.

Pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. That makes it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

To get a high-level look into the potential downsides of over or underpricing your house and the perks that come with pricing it at market value, see the chart below:

Lean on a Professional’s Expertise to Price Your House Right

So why is an agent essential in finding the right price? Your local agent has the skill and the insight necessary to find the market value of your home. They’ll use their expertise to determine a realistic listing price by assessing:

The prices of recently sold homes

The current market conditions

The size and condition of your house

The location of your house

Bottom Line

Pricing your house at market value is critical, so don’t rely on guesswork. Let’s connect to make sure your house is priced right for today’s market.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link